When it comes to securing your family’s future, Term Insurance is one of the most powerful and affordable tools available. But here’s the confusion most people face:

Should I buy a Pure Term Plan or go for a Return of Premium (ROP) Plan?

Let’s break down both options in a simple, detailed way so you can make the best decision for your needs.

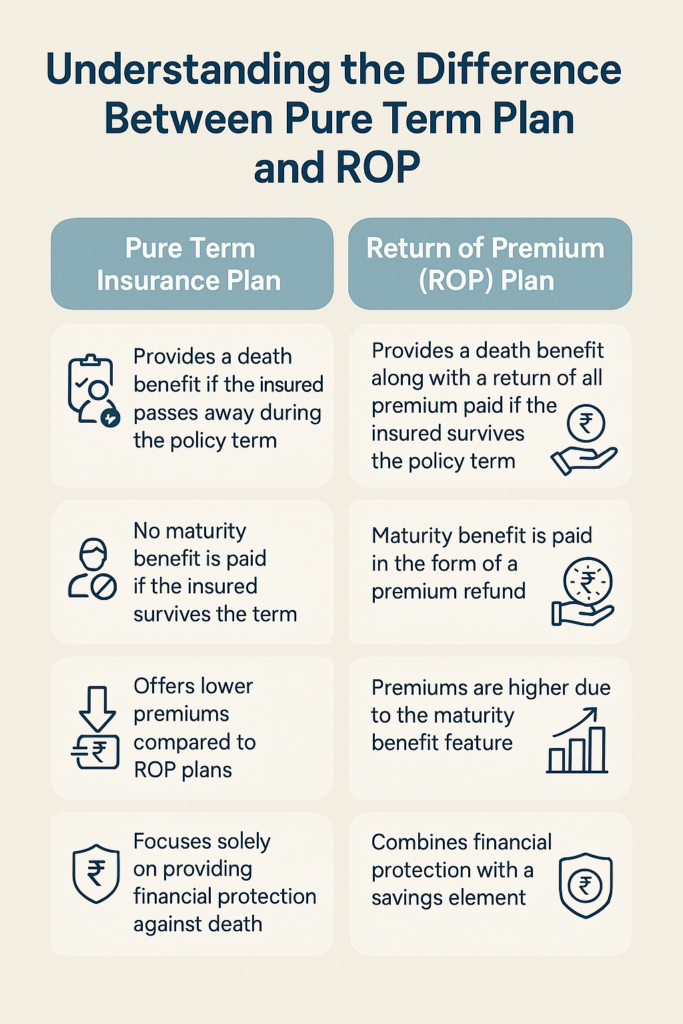

🔍 What is a Pure Term Plan?

A Pure Term Plan is a life insurance product that provides only life cover.

You pay a low premium, and your nominee gets a lump sum amount if you pass away during the policy term.

If you survive the term, you get nothing back.

✅ Key Features:

Low Premiums

High Coverage

No Maturity Benefit

🧾 Example:

Rahul, aged 30, buys a pure term plan of ₹1 Crore for 30 years.

He pays ₹10,000 annually.

If he dies in the 15th year → Nominee gets ₹1 Crore.

If he survives all 30 years → No money is returned.

🔁 What is a Return of Premium (ROP) Plan?

An ROP Plan also provides life cover, but with one major difference:

If you survive the policy term, you get all your premiums back.

It’s like combining insurance + savings (though no interest is paid on your returns).

✅ Key Features:

Life cover like term plan

All premiums returned on survival

Higher premiums than pure term plan

🧾 Example:

Rahul, aged 30, buys an ROP plan of ₹1 Crore for 30 years.

He pays ₹25,000 annually.

If he dies in the 15th year → Nominee gets ₹1 Crore.

If he survives 30 years → Rahul gets ₹7.5 Lakhs back (₹25,000 × 30 years)

📊 Comparison Table: Pure Term vs ROP Plan

| Feature | Pure Term Plan | ROP (Return of Premium) Plan |

|---|---|---|

| Premium Cost | Low | High |

| Life Cover | Yes | Yes |

| Money Back on Survival | No | Yes (Total Premiums Paid) |

| Maturity Benefit | No | Yes |

| Ideal For | Pure protection seekers | Protection + return seekers |

| Flexibility | High | Limited |

| Tax Benefit | Yes | Yes |

🎯 Who Should Choose What?

👉 Choose Pure Term Plan if:

You want maximum life cover at lowest cost

You are okay with no returns

You want to invest separately for wealth creation

👉 Choose ROP Plan if:

You prefer getting something back at the end

You are okay with paying more premium

You want a guaranteed return (without interest)

📈 Illustration: Cost & Benefit Comparison

Let’s assume both plans are for 30 years with ₹1 Crore sum assured.

| Plan Type | Annual Premium | Total Premium Paid | Payout on Death | Payout on Survival |

|---|---|---|---|---|

| Pure Term Plan | ₹10,000 | ₹3,00,000 | ₹1 Crore | ₹0 |

| ROP Plan | ₹25,000 | ₹7,50,000 | ₹1 Crore | ₹7,50,000 |

💡 In ROP, you get back your premium – but remember, no returns, interest, or bonus is added.

📝 Final Thoughts from Reassure101

At Reassure101, we believe that the best insurance policy is one that suits your life goals and budget.

If you are focused on protection at minimal cost, go with Pure Term Plan.

If you like the idea of getting your money back, an ROP plan might give you peace of mind.

👉 Need help choosing the right plan?

📞 Call us at 7045965663 or visit 🌐 www.reassure101.com for a free consultation with our experts.